Roof Improvements Depreciation Years

Part Three The Value Of Accurate Roof Age In Claims

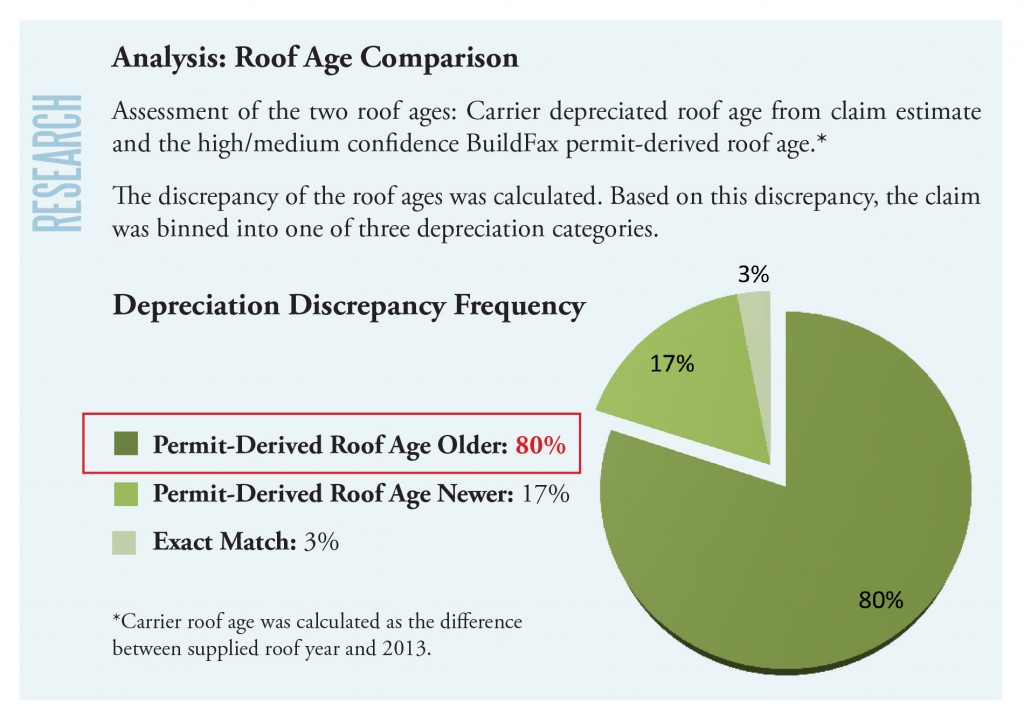

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

Guide To Expensing Roofs Expense V Capitalization Section 179 D Kbkg

Did You File A Hail Claim In 2020 Roof Damage Repair Roof

Roof Leaks Tips For Filing A Roof Insurance Claim Roofing Residential Roofing Roofing Contractors

Section 179d Tax Deduction For Commercial Roof Replacements

A roof system is a major component because it performs a discrete and critical function in a building structure.

Roof improvements depreciation years.

What Is The Depreciation Of The Roof On A Commercial Building

Mjulzmdcnmjbzm

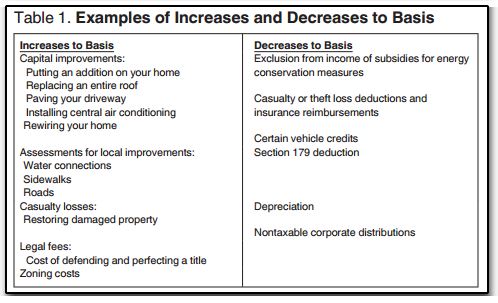

12762 Increasing Basis On An Asset Being Depreciated

Do You Know About How Your Insurance Value Is Calculated Insurance Claim Insurance Understanding

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

Roof Insurance Acv Vs Replacement Cost Bankrate

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Tax Depreciation Schedules Australia Is An Accounting Procedure Where The Amount Of Value Left In Each Fragment Of Equipmen Schedule Service Australia Schedule

Home Business Computers 130 20200411031517 49 Home Business Hawaiian Attire For Boys Your Home Is My B In 2020 Inexpensive Home Decor Cabin Home Improvement Blogs

Xactimate And Insurance Prices Change Every Month Do You Know How Much Www Overheadandprofit Com Insura American Family Insurance Liberty Mutual Fire Damage

179 Tax Deduction For Commercial Roofing Projects Advanced Roofing Inc

Home Business Job Ideas 354 20190401102827 49 Home Based Small Business Opportunities Building A Garage Home Improvement Projects Best Home Based Business

Rule The Roost With These Fun And Creative Home Improvement Tips Vacation Home Decor Direct Home Buying Tips

Camscanner In 2020 Understanding How To Make Sheet Music

Decor Your Home In Style Gutters Seamless Gutters Roofing

Roof Damaged By Wind Roof Restoration Roofing Services Roof Damage

How Bonus Depreciation Affects Rental Properties Millionacres

Pin On Home Guides

Pin On Quality Pins

Source : pinterest.com